Summary

- Vistry has transitioned from a traditional housebuilding to a partnership only model positioning itself as the UK leader in affordable housing.

- Labour’s ambitious housing goals and policies, such as mandatory housing targets, fiscal stimulus and green/brown belt reallocation, align directly with vistry’s expertise.

- Recent cost overruns tied to the legacy housebuilding division have impacted near term financials. However, these issues are isolated, and the partnership business remains unaffected.

- In-house timber frame production, bulk material purchasing, and economies of scale further enhance cost efficiency, supporting long term profitability and competitive advantages.

Business

Vistry is a UK housebuilder which has historically operated in two primary business models: traditional housebuilding and partnerships. However, approximately a year ago, the company began phasing out its legacy housebuilding division to focus entirely on its partnership business. This transition is still underway, and Vistry has stopped reporting the two segments separately.

While other companies also employ the partnership model, Vistry is the clear leader in the sector now. In 2024, the company expects to deliver circa 17,500 homes. In contrast, Lovell and Keepmoat delivered 3,000 and 4,100 homes respectively in 2023.

Vistry’s scale and focus on the partnership model position it as a dominant player in the affordable housing space.

A fitting comparison for Vistry’s new model is the US-based homebuilder $NVR, a pioneer of the capital-light approach. A quick glance at NVR’s stock chart and outstanding shares since inception highlights its success in value creation. A former board member of NVR is now on Vistry’s board to help them with this strategic shift.

Additionally, the capital freed up by this transition would let the company return £1 billion in excess cash to shareholders, with another £300 million going to reduce the debt. £200 million of this buyback target has already been completed.

Moreover, beyond an initial buyback, management anticipates capital returns to amount to 50% of the operating income. With a near-term target of £800 million operating income, Vistry could return a significant amount back to shareholders via NVR-style buybacks.

Historical Timeline

Vistry, as it is known today, was officially formed in 2019 through the merger of Bovis Homes and Galliford Try’s housing division. Greg Fitzgerald, the current CEO, was previously the CEO of Galliford Try between 2005 and 2015, during which time the company grew substantially, including a significant expansion of its partnership business. After briefly serving as a chairman, he retired in 2016.

By 2017, Bovis Homes faced serious challenges. Fitzgerald, with his strong track record at Galliford Try, was brought out of retirement to rescue the struggling company. Under his leadership, Bovis recovered and was back on track in two years, and shortly thereafter, they acquired Galliford Try’s housing business.

However, it was the 2022 merger with Countryside Partnerships that truly shaped the Vistry we see today.

Before the pandemic, Countryside Partnerships was a shining example of the partnership model. By 2019, they were delivering 4,400 homes annually. Their partnership division, which accounted for roughly half of their profits, boasted a remarkable ROCE of 78%, far exceeding the typical 15-25% range for UK housebuilders. Despite these achievements, the market undervalued Countryside, granting it a P/E multiple of 10—lower than many peers. This reflected the market’s emphasis on valuing housebuilders by book value rather than earnings, penalizing those with higher returns on equity.

In response, then-CEO Ian Sutcliffe announced plans to split Countryside into two entities to unlock shareholder value. Unfortunately, the CEO had to step down due to personal reasons, and the new management scrapped the plans of a split, which left shareholders frustrated, attracting activist investor Brown West, which acquired a 10% stake and secured a board seat. Over the next year, the board and top executives resigned, and the board committed to a pure-play partnership business. Later, the company decided to sell, and in September 2022, Countryside agreed to a stock-for-stock merger with Vistry, creating the entity we recognize today.

The merger was largely successful. Management exceeded initial estimates for cost savings, and the stock price more than doubled following the merger. By September 2023, Vistry announced its decision to focus solely on partnerships, signaling a definitive shift in strategy.

Since then, the company has been winding down its non-partnership business, completing existing projects, reallocating suitable plots to the partnership division, and selling off the rest. This process is expected to free up approximately £1 billion in capital, of which £200 million has already been returned through buybacks and dividends.

However, challenges emerged in October 2023 when Vistry disclosed cost understatements amounting to £115 million on several sites. This revelation caused the stock price to plummet from £13 to £9.5. A month later, an additional £50 million in losses were identified, and the profit outlook was reduced from £350 million to £300 million, allocating 50% of the reduction to these one-time losses and the remaining to a slowing economy. This took the share price down to the present level of £6.3.

Despite these setbacks, there are reasons to believe that the market may be misinterpreting the implications of the issues, a topic we’ll explore in detail.

Partnership

Vistry’s partnership approach differs significantly from the traditional model used by most housebuilders. It involves collaborating with housing associations, local authorities, and private rental sector (PRS) investors to deliver a mix of affordable, PRS, and privately sold homes.

The structure of these partnerships varies by project. In some cases, the developer provides the land and allocates the units to partners. In others, partners such as housing associations might own the land and bring in Vistry to develop it. In either case, partners usually prepay for the units before the construction begins.

The traditional housebuilding process is well understood: developers identify a site, secure necessary approvals, and either purchase the land outright or via an option contract. Construction of individual homes typically takes 5 to 7 months. However, the partnerships model is a fundamentally different approach, emphasizing collaboration between homebuilders and public or private entities such as local governments or housing authorities.

In the partnership model, the developer forms a joint venture (JV) or enters into a contractual agreement with the public entity. These collaborations leverage resources and align objectives to deliver housing that meets both social and commercial needs. For example, Vistry may develop on donated land without forming a separate entity while still operating under principles of shared responsibility and benefits.

The partnership model enables efficient development by distributing risk, leveraging resources, and aligning incentives. It represents a shift from the speculative approach of traditional housebuilding to a collaborative framework designed to meet the needs of diverse stakeholders, including local communities.

Below are common structures of partnership JVs:

Development-Led Joint Venture

In this model, a local authority partners with a developer to purchase land, often receiving a cash payment upfront. The agreement specifies a timeline for the developer to complete construction on the site. Once the project is finished, the local authority receives a share of the profit.

Investor-Led Joint Venture

Here, a long-term investor such as a pension fund or real estate trust provides forward funding for a development and shares in the project’s financial risks. The local authority assumes the long-term operational risk for the completed development. Typically, the investor leases the land from the local authority and finances the construction with a homebuilder. Upon completion, the local authority leases back the homes from the investor for an agreed term. At the end of the lease, ownership of the asset reverts to the local authority, often for a nominal payment.

Limited Liability Joint Venture

This type of JV is established on a project-by-project basis. Local authorities may also secure strategic partnerships with developers to ensure continuity across multiple projects. Upon completion, the council and its partner may either retain or sell the completed assets. Retained properties may be transferred to the council’s housing company, an investor, or a new JV formed for long-term management.

Return on Capital and Moat

The partnership model stands out for being capital efficient offering significant advantages to traditional housebuilding. A developer traditionally spends years acquiring land, navigating planning waiting for sequential sales and then building. Even with a strong margin ROIC is very low.

In partnership model homes are often presold 1-2 years in advance. Pre-selling eliminates the need to delay construction for market timings. The land is often provided by the partners with planning permissions already in place.

In 2023 Vistry achieved a 21% return on capital which was dragged down by their former housebuilding business. Their partnerships business was delivering ROCE around 40%.

Management aim for 40% ROCE overall by 2028, driven by wind down of traditional housebuilding business and further synergies from merger with countryside.

Unlike the private housing market, which is highly sensitive to the economic factors like interest rates and consumer confidence, partnerships are far more stable. This is because the buyers are housing associations and PRS investor which have long term objectives. This causes contractors to prefer working with vistry and bulk purchasing of materials causing economies of scale.

By 2026, Vistry’s in-house timber frame manufacturing will support 12,000 units annually further driving cost efficiencies.

Vistry has a very strong reputation with the local authorities particularly through its countryside brand which has established itself as the most reliable partner in the industry. Bellway as an example has exited the London partnership market owing to the market pressures, unable to match vistry’s capabilities.

Overall Vistry’s partnership model combines capital efficiency, resilience to economic cycles and unmatched track record. These strengths supported by economies of scale and strong institutional relationships, position vistry as the clear leader with a possible moat in the growing partnership market.

UK Housing Economics

Looking at the demand side the previous government estimated in January 2024 that 300,000 new homes are required each year. However, some suggest that this number could be higher. One report in 2019 from National Housing Federation estimated around 340,000 new homes needed while Financial Times analysis from earlier this year estimated 421,000 new homes or even as high as 529,000 new homes if current migration levels hold.

Now onto the supply side, we see a report from the govt. earlier this year where they report a total of 234,000 net new dwellings in 2022-2023, which were 6% lower than the 2019-2020 peak.

These figures suggest a severe shortage of houses, even more for the affordable houses where the demand is estimated to be 145,000 houses and supply stands at around 60,000 per year. One estimate from last year states that Britain today has a backlog of 4.3 million new homes that are missing from the national housing market as they were never built. This housing backlog is increasing each year with the mismatch in demand/supply metrics. It can take decades to fill even if the current target to build 300,000 new homes a year is reached.

The newly elected labour government has set an ambitious target of delivering 1.5 million new homes over the next five years. Skepticism around this target is understandable particularly given the conservative governments failure to meet their promise of delivering 300,000 homes annually by 2024. Building more housing was unpopular in many conservative strongholds which led them to drop the target of delivering 300,000 new homes.

Labour, however, enjoys a strong electoral mandate and is less constrained from voters resistant to new development in local areas and the party’s majority in the parliament makes it easier to implement necessary reforms.

Early signs of progress

Labour has already introduced several policy changes aimed at kickstarting housing developments, including

Mandatory local housing targets: Replacing advisory targets with mandatory ones. Local Planning Authorities (LPA’s) are now required to meet the targets or risk intervention by the government.

Revised target calculations: Adjusting the calculation methodology for housing targets which should increase them by roughly 21%.

Selective green belt reallocation: Allowing development provided that at least 50% of the units are affordable housing.

Expanding Definition of Brownfield Lands: Broadening what qualifies as previously developed land to make more areas available for housing

Additional Funding: Allocating an extra GBP 500 million to the Affordable Homes Program (AHP)

Greg Fitzgerald, Vistry’s CEO commented on Labour’s commitment during the recent earnings call:

“So, Labour in the run-up to the election talked a lot about housing. They could have said that after winning the election, only joking, it’s business as usual. What they haven’t done is they have absolutely — and I’ve never seen, and I’ve been doing this for 43 years, nothing like it, whether it’s meetings, letters to local authorities, to housing associations, to us, they mean business.”

While Greg’s optimism can be viewed skeptically, Labour’s actions so far have aligned with their stated intentions, signaling a strong push toward their housing goals.

The private housing market is unlikely to derive significant growth. Unlike affordable and PRS developments which are constrained by planning and funding, the primary limitation in the private market is demand.

The real opportunity lies in affordable housing and the PRS. Even if private sales grow by 25%, affordable and PRS housing would still need to double to meet Labour’s targets. This presents a major medium term or even long-term growth opportunity for Vistry if the funding remains consistent, particularly given its leadership in affordable housing projects and large scale developments.

Cost Overruns

On October 8, 2024, Vistry revealed that the full life cycle cost on nine of its approximately 300 developments had been understated by about 10%, leading to a £115m impact, spread over the next three years. This issue was isolated to the south division of the legacy business and the management responsible has been replaced. Despite these actions the market reacted sharply. Stock fell from £13 to approximately £9.6.

Vistry then engaged an external auditor to conduct a comprehensive forensic review of all 300 sites. The audit uncovered additional cost issues in a few more developments, also within the south division, adding £50m to the total impact. Stock declined further dipping below £7.

Contrary to many reports that suggested these issues could point deeper flaws in vistry’s partnership model and that the costs overruns might be much more, the auditors report confirmed that these issues were only isolated to vistry’s legacy business and were confined in the south division. However, market’s reaction didn’t significantly change even after this clarification was made public.

One of the other important news released with this was the sales/trading statement in which vistry lowered the outlook of operating profit from £350 to £300m, half of this was because of these one-time cost adjustments and the other half was because of the slowing economy. The number of homes completions were previously expected to be more than 18,000, they were cut to around 17,500. Company also explained that the timeline of the return targets set will also increase. Exact timeline is not announced yet.

This cut in outlook increased the pessimism on the already beaten down stock of vistry. Market seems to be waiting for the next years outlook and timeframe of the returns.

The independent review attributed the problems to insufficient management capability, non-compliant forecasting processes and poor divisional culture. This boils down to the mid-level management in the south division whose leadership came exclusively from vistry’s legacy business, which is being wind down anyways.

The independent review confirmed that no similar issues – financial, cultural or procedural exist in other divisions.

Insider buying following the stock dump has been noticeable. On the day of the first disclosure CEO Greg Fitzgerald purchased gbp200k in shares and two independent directors who had never previously invested bought 75k and 45k. Browing west, Vistry Largest shareholder and controlled by Usman Nabi, who also hold a board seat increased their stake by £7.5m worth of shares and a further £3.65m following the second announcement.

The financial impact is significant but not catastrophic. Most of the cost adjustments will affect FY24, reducing pre-tax profits by £105m, FY25 by £50m, and FY26 by £10m.

Valuation

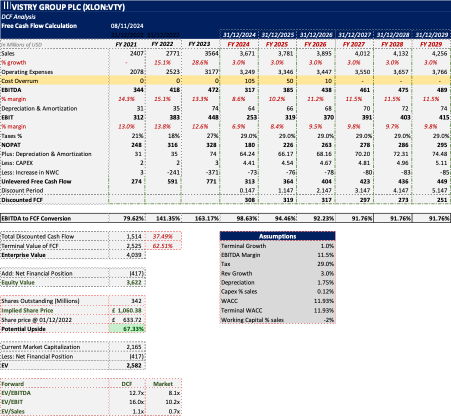

We have employed a discounted cash flow model for the valuation purposes. In this free cash flow model we have tried to remain as conservative as possible and not to rely on the managements guidance for growth and margins. As the Labour government has promised to deliver growth in the housing sector and has already taken steps to deliver on their promise so we have used a 5 years’ time frame to reflect the labour governments tenure. We could use a longer time frame as the shortage of houses will take longer than a decade to resolve but we are not sure of the future governments policies, so we decided to only look at the near future where we have clear stimulus from the government.

In that regard Vistry is guiding for a 5-8% near term growth but we have used only 2% growth which is not just conservative, it also doesn’t align with our whole discussion but the point of the DCF is to find how company performs on very stressed assumptions.

Ignoring the long term deficit of houses and vistry’s prime position to capture that market I have used only 1% terminal growth. The operating margins are expected to be lower in the partnership business and given the economic outlook, increasing mortgage rates, and decreasing consumer affordability, company might have to spend more on marketing. Although going forward in the partnership model just 25% roughly will be sold to the private market so the deteriorating economic conditions will not have much impact on the margins and marketing needs will be lower. The straight-line EBITDA assumption we have used is 11.5% but this doesn’t account for the cost over runs. Adjusting for this result in EBITDA ranging from 8.7% to 11.5%.

Vistry has had negative working capital requirements ever since the countryside acquisition because of the partnership model. Going forward as vistry goes full partnership mode the working capital will be even more in the negative territory. Last two years Vistry had -9% and -10% working capital requirement as a percentage of sales. This is a huge positive for the valuation but in our DCF we will only use -2%. Capex requirements here are minimal, the average we have used is in line with the historical average but higher than the consensus. Same goes for the depreciation where we have used a historical average lower which is lower than the consensus.

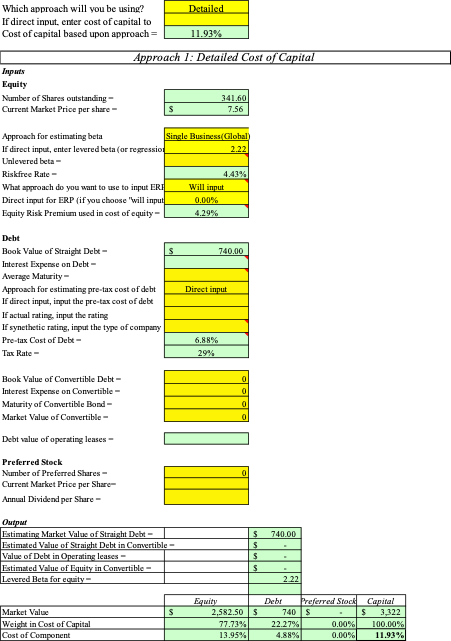

The cost of capital was calculated based on the traditional framework using CAPM for the cost of equity. We used Professor Damodaran’s current month ERP of 4.29%-, and 10-years UK GILT of 4.43% for the risk-free rate. Using the market beta of 2.22% we arrive at 13.95% cost of equity. Pre-tax Cost of debt based on the weighted average was found to be 6.88%. Based on these two figures and the respective weights for debt and equity we arrive at a cost of capital of 11.93%.

With these inputs as our base, we reach at a valuation of £10.60 which represents a 70% upside from the current levels.

It is very important to reiterate the fact the management is guiding for more aggressive numbers. Given the housing shortage and the stimulus from the government we believe those numbers will eventually be achieved but here in our valuation we have tried to find the most conservative valuation to have a sense of the margin of safety if everything doesn’t go according to the plan.

Detailed Cost of Capital

Discounted Cash Flow

Sensitivity Analysis

To aid all those with a different potential input than ours, we have performed a sensitivity analysis on the main value drivers.

In the table below, Sensitivity analysis highlights the potential valuation based on different operating margins and cost of capital as we believe both have room to improve.

Considering our use of below guided terminal growth and higher WACC, table below is useful to understand the impact different inputs can have on the valuation.

Conclusion

In summary, Vistry group is under transition to focus solely on its partnership business, abandoning its traditional housebuilding division to become a leader in the affordable housing sector. This capital light model, inspired by US based NVR offers significant advantages including higher ROIC, enhanced cashflow stability, and resilience to macro volatility. Despite recent setbacks, including cost overruns tied to its legacy business, a reduced profit outlook, these issues are isolated and do not reflect its core partnership model strengths. With growing demand for affordable housing, bolstered by the Labour government’s ambitious housing policies and vistry’s proven expertise and scale, the company is well positioned for long term growth. Insider buying and managements proactive steps to address challenges reinforce confidence in vistry’s strategy, which combines operational efficiency, government alignment, and a commitment to a substantial shareholder returns.

Vistry’ current valuation appears to offer a significant margin of safety, with the stock trading at a steep discount to its estimated intrinsic value. Risks remain particularly around the governments promises slowing economy increased taxes and the management, but the business fundamentals strong partnership model and planned shareholder returns present a compelling investment opportunity.