A company to keep into the radar although valuation looks stretched

BRIEF

- LSPD is a platform offering front-end consumer experience, back-end operations management, and a payment system.

- COVID-19 has dramatically increased the demand for the service as retailers rush to integrate online sales channels and payment systems.

- Well managed with a clear path to grow by scaling up dimensionally via M&A piggyback strategy.

- Valuation looks stretched for the time being but it’s worth looking at this company as its addressable market is huge. We would reconsider the story should the price fall back below $40 per share.

What is Lightspeed?

Lightspeed POS (TSE: LPSD / NYSE: LSPD) provides cloud-based point-of-sale and e-commerce software to restaurants, hospitality businesses, and retailers in over 100 countries. The platform’s three main pillars are the front-end consumer experience, back-end operations management, and the payment system. The company offers different services (SaaS) and hardware to run its software. They provide products for retailers like Point of sale, e-commerce, payment system, loyalty system, analytics, accounting, hardware (cashiers, scanners, printers, etc.), and other integrations.

Why did we look at the stock?

There have been certain movements related to this company. AMI Partners estimates that there are approximately 226 million small and medium-sized businesses (SMBs) around the world generating around $59 trillion of revenue in 2018. Lightspeed’s addressable market is huge and the firm is trying to consolidate the market by acquiring small operators and their client base.

Why do we believe it is overvalued?

LSPD valuation looks unsustainable under whatever metric we have tried to use. The stock is trading at around 35x P/Sales 2021E and 24x P/Sales 2022E. We understand that covid-19 has accelerated the digital transition for SMEs dramatically but, at current prices, we see more risks than upside on the story even if LSPD would continue to consolidate its market. Furthermore, we should factor in the potential dilution on equity (more likely at current prices as many growth companies are taking advantage to raise fresh money) on top of the difficulties in integrating targets being acquired. We would be keen to look at this interesting equity story once the price would fall below $40 per share.

Increased demand for services is an LPSD catalyst

It is hard for small and medium businesses to keep up with new developments in customer engagement, operation and channel management, and online payments. These kinds of retailers tend to look for modular services to keep updating their systems without incurring many complications. Lightspeed is also promising for data-driven solutions that are becoming critical for the businesses they serve. These services, as well as current and future artificial intelligence and other developments, are easy to integrate as new modules, driving further incremental revenue.

The demand for the service has dramatically increased due to the COVID-19 pandemic as retailers rush to integrate online sales channels and payment systems. However, Lightspeed’s churn rate has also increased because businesses like restaurants are suffering losses, and many have closed due to COVID-19’s impact on the real economy.

The company seems to be moving in the right direction when it comes to partnerships and acquisitions. Last February, they partnered with Stripe to add a payment module to Lightspeed’s services. This so far has represented a great strategy and a new revenue driver to the platform. Furthermore, in November, Dax Dasilva, Lightspeed’s CEO and founder announced the acquisition of ShoopKeep, a similar platform with more than 20,000 small and medium retailers in the USA. On December 1st, the company announced the acquisition of Upserve, a restaurant management cloud-software company that focuses on high-end restaurants, fast-casual, and bars.

Competitive position

The Point of Sales market is an old one and was once disrupted by offline software companies and now is being disrupted by internet-based companies.

Some Lightspeed competitors are:

- Square POS

- PayPal POS

- Heartland Retail

- Vend

- Clover

- Shopify POS

- QuickBooks POS

- Oracle Retail Xstore POS

The retail market is huge. There are approximately 226 million small and medium-sized businesses (SMBs) worldwide, generating around $59 trillion of revenue in 2018.

It is worth considering that there are a few limitations when it comes to small businesses. For instance, the price sensitivity for core software and equipment is something that the sector has to keep in mind to be able to compete. Lightspeed has very reasonable plans from just $69 to $259 per month for retailers and a starting package of $59 to $98 for restaurants. For that reason, the payment system was a good move as they entered the percentage game with much better outcomes possibilities for revenue.

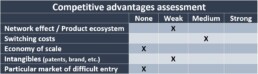

Nevertheless, we are still searching for substantial competitive advantages as only a significant moat could assure the permanence and sustained growth of Lightspeed in the market in the long run. So far, we estimate that the switching costs could represent a medium barrier to entry to competitors.

Similar to what happens with legacy cashier systems (which are being disrupted by these internet companies), changing the software with which retailers manage their clients, operations, and payments could be more challenging and complicated than it seems.

The network effect and product ecosystem could play a role when it comes to multiple-store businesses but still weak in terms of a real barrier to entry. Notice that the company could enjoy an economy of scale advantage in the hardware segment. However, as it represents a small part of the company’s revenues and is not the core product, we do not think such a moat could be achieved soon. The same goes for the intangibles, it is a remote possibility, but the firm isn’t close to it yet.

Lastly, as we already know, the market is not particularly difficult for new players to enter. Virtually anyone could enter the market as the software and development of such services aren’t rocket science anymore, especially for banks and payments platforms.

Financials and business insights

We believe that the company is currently trading far above its fair price as the current valuation is overestimating the future increases in demand for their services due to the pandemic.

However, as we have said before, this pandemic was a catalyst for technology adoption. Still, the world was already moving in that direction, and it probably won’t go back when the COVID-19 is over. It doesn’t mean, though, that the company will keep its position for a long time. That will depend on other factors, particularly on the company’s ability to develop and maintain competitive advantages.

Lightspeed is a subscription-based company. We already discussed different ways to approach these firms in the report on FUBOTV that you can find on the blog. The difference with Lightspeed is that they tend to have more long-term subscriptions because of the LSPD business’s nature.

We have to look at unit economics when it comes to Lightspeed. Remember, the trick lies in obtaining the user, maintaining it, and monetizing it in different ways. Lightspeed has great potential in this last respect. For instance, the inclusion of the payment system mentioned before was a clear signal. In recent events, they have clarified some ideas about the future in this matter. Data-driven services are the management promise for future modules to be included in the list of services. With artificial intelligence and big-data development, we think that they are right-minded to state that.

Retailers, restaurants, and hotels greatly benefit from these technologies, and there is much more to come. They also have multiple-store customers’ added side effect, meaning that one customer could have separate accounts/users (one per store). It serves in both ways because the Customer Acquisition Cost for this kind of customer is divided by the number of its users/stores.

Suppose the management is able to strengthen its platform by including new modular services and that they can keep their clients happy, so the churn rate is controlled. In that case, the ARPU could keep growing in time. This could improve the Customer Lifetime Value and Customer Acquisition Cost Ratio, increasing Lightspeed’s profitability in the long term.

Before getting deeper into the company’s numbers, we have to state that to get clients in this market, you have to get new starting clients, disrupt existing retailers that use legacy systems, or steal them from competitors. None of these options are easy.

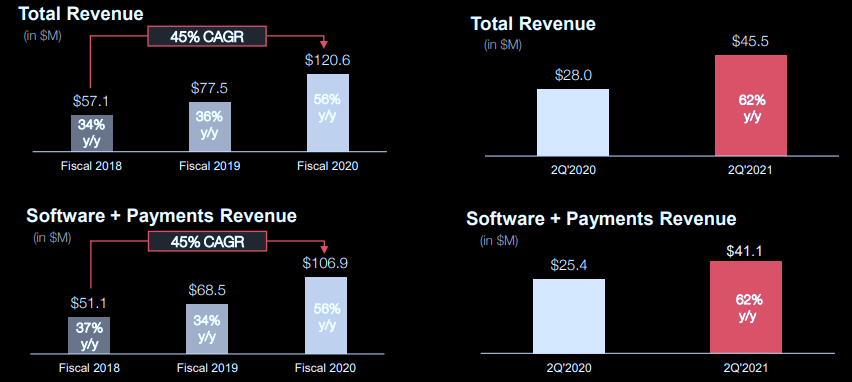

The number of users (or customer locations as they call them) has been systematically growing in the last years. The company currently has more than 80,000 users to be reported in the second quarter of 2021. A Year-To-Year growth of +40%, respecting in the same quarter of 2020.

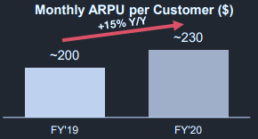

The annual Average Revenue Per User increased by 15%, which is also a good indicator and helps with our theory of a medium barrier to entry regarding switching costs. Moreover, it also speaks about Lightspeed’s capacity to increase the revenue by selling new services to existing users.

The primary revenue sources are the software (subscriptions to the different services) and the payment system (they charge 2.30% + 10/20/30 cents depending on the case). They also receive revenue from the hardware segment.

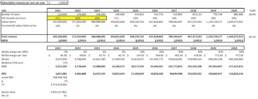

Our Valuation

We are basically repeating what we have done with FUBOTV equity story. Our goal is to find the Present value of each LSPD client. The valuation would probably be the present value of the existing and future clients’ cash flows.

For growth companies like LSPD, we continue repeating a basic concept: it is extremely difficult to have a reliable quantitative model because churn, inflation in service prices will most likely depend on the competition and on the company’s ability to scale up dimensionally.

The spreadsheet below is based on a client’s subscription base expected to grow at 26%CAGR over the 2021-30 period. We have assumed a 3% price increase, which we believe is reasonable given clients’ switching costs.

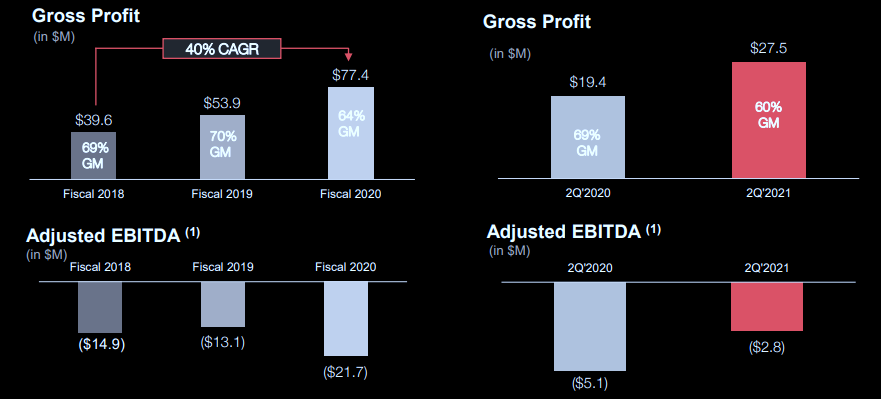

We have considered an EBITDA margin that turns positive in 2023 and stabilizes in 2030 at 50%. This means that from 2030 onward 50% of ARPU is transformed into EBITDA. This is a more than fair assumption as the business is low margin and furthermore, LSPD might incur additional costs related to the acquisitions it has done and it will do in the future.

The other key assumption we have made is that 70% of the Ebitda is converted into FCFE (Free cash flow to equity, residual to shareholders) which can finally be discounted at an appropriate cost of equity to figure out the equity value.

We have used a 9% cost of equity and a 3% perpetual growth rate. We could have done a more in-depth analysis of the beta and rely on a capital asset pricing model (CAPM). However, we believe it would not make much sense at this stage because the CAPM fails to deliver a reasonable cost of equity in cases like LSPD where basically the correlation to the index is limited as the company was listed last April.

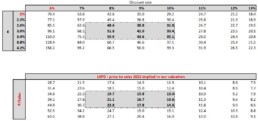

So, in table 2 we have decided to rely on a sensitivity analysis which calculates the price per share by changing the cost of equity and the perpetual growth rate (g). Assuming a discount rate between 8% and 10% and a perpetual growth rate between 2.6% to 3.4%, the average price could be between $32 and $56 per share. The downside here is around 20%!

We have also checked the 2022 P/sales ratio implied by our sensitivity. In other words, still in table 2, we show for each equity value (or price per share) which is the implied 2022 P/sales. At current prices LSPD is trading around 35x P/Sales 2021E and 24x P/Sales 2022E. Our fair value range between $32 and $56 per share implies between 13x and 22.8x P/Sales 2022E.

In our view, there is evidence enough to consider LSPD overvalued: low margin business, low entry barrier, potential dilution on equity are all factors we have to take into consideration. If we were not in a pandemic scenario that is accelerating the digital transition, our valuation would have been even more conservative.

Spreadsheets

Table 1: DCF model

Table 2: Sensitivity analysis and 2022 implied P/E sales

About Antonio Velardo

Antonio Velardo is an experienced Italian Venture Capitalist and options trader. He is an early Bitcoin and Ethereum adopter and evangelist who has grown his passion and knowledge after pursuing the Blockchain Strategy Programme at Oxford University and a Master’s degree in Digital Currency at Nicosia University.

Velardo manages an 8-figure portfolio of his investment company with a team of analysts; he is a sort of FinTweet mentor, people interact with him online, and he has more than 40,000 followers after his tweets. He has built a fortune in the great tech years and put together a tail strategy during the pandemic that allowed him to take advantage of the market drop. “I did not time the market, and I did not think this was even a black sworn,” he says.

On the side of the financial markets, Velardo has a unique combination. He was a real estate entrepreneur that developed several projects in Tunisia, Miami, Italy, the UK, and many other countries and cities. But he has always been passionate about options trading. Still, contrary to the volatility player and quant trading, he always had a value investing touch in his blood. Antonio studied Value Investing at Buffet’s famous business school at Columbia University. Even though the central concepts of value investing are antagonists to the venture capital pillars, Antonio’s approach tries to bridge elements of both worlds in order to seek alpha. Velardo has learned the importance of spotting pure growth stories and taking advantage of their S-Curve position. This is an essential element of Velardo’s approach as he looks forward to embracing great tech stories at the right time of the adoption cycle. This applies to stocks but also to blockchain projects.